Expert insights from Angie Trocke, VP Commercial Banker at Highland Bank

For many business owners, real estate is more than a place to operate—it can be a strategic investment in the future. Whether purchasing a building, expanding into a new space, refinancing an existing property, or exploring income-producing investment opportunities, Commercial Real Estate Financing can help businesses create stability, support growth, and build long-term value.

At Highland Bank, commercial real estate financing begins with understanding each client’s goals and helping them navigate opportunities with clarity and confidence. With more than twenty years in the banking industry, Angie Trocke helps business owners evaluate how real estate ownership can support both their current needs and long-term vision.

“Commercial real estate ownership can provide added value to a business owner’s overall objectives and long-term success.”

Financing That Supports Growth and Opportunity

Commercial real estate financing can support a wide range of business needs, from purchasing a property for your own operations to financing investment real estate that generates rental income. While each scenario is unique, the overarching goal is often the same: creating opportunities for growth while building long-term value through property ownership.

Angie works with businesses across many industries and believes commercial real estate ownership can be a valuable option for a variety of organizations. For some business owners, owning their space provides greater control and flexibility. For others, real estate becomes an additional income-producing asset that can continue generating revenue long after they step away from day-to-day operations.

Some of the most rewarding commercial real estate projects arise when a business is ready to take the next step. Angie recalls helping a growing company that had outgrown its leased location and needed additional space to support expansion. Through commercial real estate financing, the business was able to purchase and renovate a larger property, creating room for future growth while building equity in a valuable long-term asset.

She has also helped businesses purchase buildings that they previously leased, giving owners greater control over their future and helping them avoid the uncertainty that can sometimes come with changing landlords, redevelopment plans, or relocation pressures. In these situations, access to the right financing and guidance can make all the difference.

Preparing for Financing and Planning Beyond the Purchase Price

Successful commercial real estate financing often begins well before a purchase agreement is signed. Angie encourages business owners to start by having conversations with their banker, accountant, and financial advisor to better understand equity requirements, cash flow expectations, and the financial commitment associated with property ownership.

Businesses that are best positioned for financing typically demonstrate healthy liquidity, adequate cash reserves, and a clear plan for the property. Depending on the project, documentation such as tenant leases, operating statements, and property expense details can help create a smoother approval process and provide a clearer picture of the opportunity.

It’s also important to plan beyond the purchase price itself. Property taxes, insurance, utilities, maintenance expenses, and future capital improvements all play a role in long-term ownership costs. Factoring these expenses into projections early can help business owners make informed decisions and avoid unexpected surprises down the road.

What Business Owners Should Know Before Getting Started

Commercial real estate financing often differs from what business owners expect based on their experience with residential lending. Commercial loans are typically structured differently, with shorter amortization periods and financing terms that are tailored to the property, the borrower’s goals, and the long-term strategy for the investment. Understanding these differences early can help business owners make more informed decisions throughout the process.

Borrowers frequently have questions about required equity, repayment terms, and financing flexibility. Angie emphasizes that these conversations are most productive when they happen early. Understanding a client’s plans for the property helps ensure the financing structure aligns with their goals and supports both short-term needs and long-term success.

A Relationship-Driven Perspective on Commercial Real Estate

Strong commercial real estate financing starts with open communication, clear expectations, and a trusted banking relationship. Angie believes clients should understand every step of the process—from appraisals and title work to financing proposals and documentation requirements. Frequent communication helps keep projects moving forward and allows business owners to make decisions with confidence.

Many of Angie’s conversations begin long before a client is ready to purchase a property. Those early discussions help business owners better understand what lenders look for, identify opportunities for improvement, and prepare financially before the right property becomes available. By providing education and guidance from the start, she helps clients approach commercial real estate ownership with greater clarity and confidence.

Take the First Step Toward Your Next Business Opportunity

Whether you’re considering purchasing your first commercial property, expanding into a larger space, refinancing an existing building, or exploring investment real estate opportunities, you don’t have to navigate the process alone. At Highland Bank, commercial banking is grounded in relationships, local decision-making, and thoughtful conversations that begin with understanding your goals—not just your numbers.

By working with Angie Trocke and the Highland Bank commercial banking team, business owners gain a trusted partner who can help evaluate opportunities, prepare for financing, and determine how commercial real estate ownership can support what’s next. If you’re ready to start the conversation, connect with Angie today.

Heading off to college is an exciting new chapter—new friends, new experiences, and for many, your first taste of financial independence. While managing your money might feel a little overwhelming at first, building smart habits now can make your college experience a lot less stressful and set you up for success long after graduation.

Before You Leave: Set Yourself Up for Success

Before move-in day, take time to get a clear picture of your finances. Start with a simple budget so you know how much money you’ll have available and how far it needs to stretch throughout the semester. Think through expected costs like textbooks, meals, transportation, subscriptions, and everyday spending.

It also helps to set up the right tools ahead of time. Opening both a checking and savings account allows you to keep your spending money separate from what you want to save, making it easier to stay disciplined.

A few additional tips to feel more prepared:

Build a small emergency fund for unexpected expenses

Set up direct deposit if you’ll have a part-time job

Download a budgeting or banking app so you can track spending easily

Talk through financial expectations with family so you know what you’re responsible for

A little preparation now can give you a lot more confidence once classes begin.

While You’re at School: Stay on Top of Your Money

Once you’re on campus, your financial routine becomes part of your everyday life. The key is consistency. Checking in on your spending regularly, whether weekly or monthly, can help you stay within your limits and avoid surprises.

Start by prioritizing essential expenses like groceries, rent, and school supplies. Then, plan ahead for non-essentials like eating out, streaming services, and weekend plans. Having this awareness helps you make smarter choices without feeling like you’re missing out.

You can also make things easier by building simple habits into your routine:

Set spending alerts so you always know your balance

Use a budgeting app to categorize expenses automatically

Automate transfers to savings—even small amounts add up

Revisit your budget each month and adjust as needed

Even saving a little each week can create a helpful cushion and reduce stress when unexpected costs pop up.

Get Rewarded with the Right Checking Account

The right checking account can do more than just help you manage your money—it can actually reward you for it.

With a Kasasa Cash Back® checking account, you can earn cash back on everyday purchases simply by using your debit card. The qualifications to earn rewards each cycle are straightforward and typically include things you’re likely already doing—like making a certain number of debit card purchases, having a direct deposit, and enrolling in eStatements.

There are no monthly maintenance fees and no minimum balance requirements, which makes it a great fit for student budgets. And even if you don’t meet the qualifications during a given cycle, your account is still completely free—you just won’t earn rewards that month.

It’s simple, flexible, and designed to fit into your everyday life—so you can focus on school while your account works for you.

Banking That Keeps Up With You

College life moves fast, and your banking should keep up. With mobile banking, debit cards, and mobile wallets working together, managing your money becomes quick, easy, and built around your schedule.

Mobile banking lets you check your balance between classes, transfer money in seconds, deposit checks from your phone, and track your spending in real time. You can also set up account alerts to notify you about things like low balances, large purchases, or unusual activity—helping you stay informed and avoid surprises without constantly checking your account. Many students rely on these tools because they make staying organized effortless and accessible anytime, anywhere.

Pair that with your debit card, and you have a simple way to stay on budget since you’re spending money directly from your account—not borrowing it. This helps you avoid overspending and build strong financial habits early.

For even more convenience, you can add your debit card to your mobile wallet (like Apple Pay or Google Pay). This allows you to make fast, secure, contactless payments with just your phone—perfect for grabbing coffee, paying for groceries, or making quick purchases on the go.

Together, these tools give you more visibility, control, and confidence—so your money keeps up with your life, not the other way around.

Small Habits Now, Big Benefits Later

College is the perfect time to build strong financial habits that will stick with you for years to come. By planning ahead, budgeting smartly, and using tools that make money management easier, you can stay in control and feel confident in your finances—no matter what your schedule looks like.

Ready to Get Started?

Open a Kasasa Cash Back® checking account today and start earning rewards for the things you already do—like using your debit card and managing your money on the go.

Visit your nearest Highland Bank location or connect with us to get started.

Expert insight from Janelle Higgins, Vice President Commercial Banker at Highland Bank

Growth rarely happens by accident. For business owners, it’s often the result of making strategic investments at the right time—investing in equipment, managing cash flow intentionally, and having access to capital when opportunity arises. When used thoughtfully, working capital lines of credit and equipment financing can do more than solve short‑term challenges—they can help businesses move forward with confidence and take their business to new heights.

At Highland Bank, these financing tools are designed to support both stability and long‑term growth. VP, Commercial Banker, Janelle Higgins, shares real-world insights from her experience working with business owners across a wide range of industries. She has seen firsthand that having access to the right financing can be transformative.

“I’ve seen clients start at a couple million in sales and triple their revenue in just a few years by having access to working capital and equipment financing.”

Financing That Keeps Businesses Moving Forward

Working capital lines of credit and equipment loans play different roles, but together they create a strong financial foundation.

A working capital line of credit helps businesses manage short‑term operating needs. It’s commonly used to bridge timing gaps—when expenses come due before receivables are collected or inventory has turned into cash. Rather than slowing operations during busy or seasonal periods, a line of credit provides flexibility and peace of mind.

Equipment financing supports longer‑term investment. These loans are directly tied to equipment purchases and are typically structured around the useful life of the asset. Financing equipment allows businesses to improve efficiency, expand capacity, or add new capabilities without tying up cash that may be needed elsewhere.

Turning Opportunity Into Momentum

In Janelle’s experience, businesses most often explore working capital and equipment financing during key moments; periods of rapid growth, seasonal fluctuations, or when aging equipment begins to hinder productivity. In many cases, new equipment enables businesses to take on work they couldn’t manage before, while working capital ensures cash flow keeps pace with expansion.

Importantly, having access to capital doesn’t mean it has to be used constantly. For many businesses, simply knowing funds are available creates confidence and flexibility. These tools act as a bridge, helping businesses respond quickly to opportunity, navigate uncertainty, and stay focused on long‑term goals.

Preparing for Financing—and Positioning for Success

Successful financing outcomes often begin well before an application is submitted. Businesses that are best positioned for working capital or equipment financing typically show steady or growing revenue, consistent cash flow, and a proven ability to service new debt.

Preparation plays a critical role. Thoughtful financial projections help business owners—and their bankers—understand where the organization is headed. Working capital lines are intended for short‑term needs, so discipline around usage is important. Equipment investments, meanwhile, benefit from careful consideration of break‑even timing and long‑term cash flow impact.

Clear financial documentation and proactive conversations can make the process smoother and more strategic. Even businesses that aren’t quite ready yet can benefit from early guidance to understand what steps will help them prepare.

Clearing Up Common Misconceptions

One of the most common misconceptions around working capital financing is that using a line of credit reflects negatively on the business. In reality, banks view thoughtful line usage as a normal and healthy part of a company’s cash flow cycle—not a sign of trouble.

Business owners also frequently have questions about structure. Working capital lines typically carry floating interest rates and are reviewed annually, while equipment loans often feature fixed rates and terms that vary based on the asset. In many cases, a substantial portion of an equipment purchase can be financed, allowing businesses to preserve liquidity while still investing in growth.

A Relationship‑Driven Perspective on Business Banking

With more than 25 years of commercial banking experience, Janelle Higgins brings a relationship‑first mindset to serving a variety of businesses. Her approach is grounded in listening, transparency, and helping business owners think through both immediate needs and long‑term strategy.

For Janelle, the strongest outcomes come from trust and open dialogue, often before decisions are finalized.

“The best banker‑client relationships are built on trust and transparency—on both sides.”

By encouraging early conversations and honest collaboration, she helps clients preserve liquidity, avoid unnecessary strain, and use financing as a strategic tool rather than a last resort.

Take the First Step Toward What’s Next

Whether you’re navigating growth, managing cash flow, or considering an investment in new equipment, you don’t have to figure it out on your own. At Highland Bank, commercial banking is grounded in relationships, local decision‑making, and thoughtful conversations that start with understanding your business—not just your numbers. By working with Janelle Higgins and the Highland Bank commercial banking team, business owners gain a trusted partner to help explore options, ask the right questions, and determine what type of financing can support what’s next.

If you’re ready to explore working capital lines of credit or equipment financing, take your business to new heights with Janelle Higgins and the Highland Bank commercial banking team today.

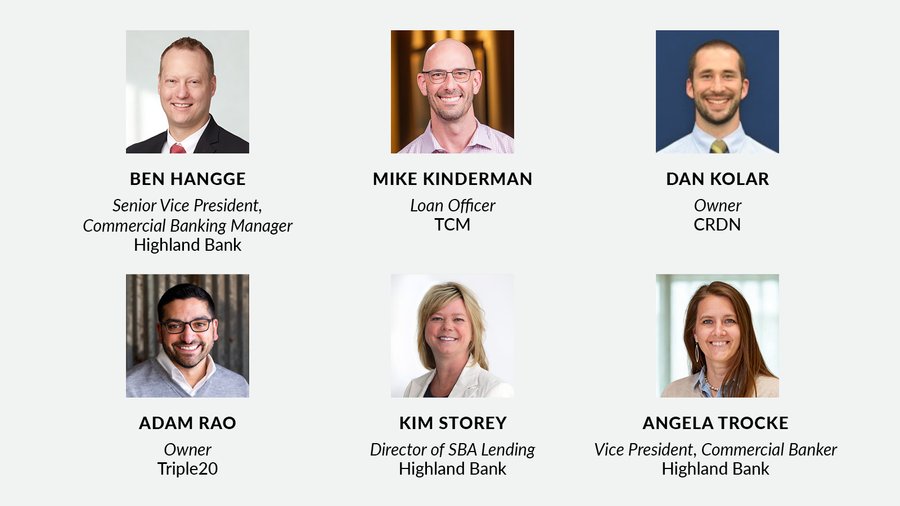

The Minneapolis-St. Paul Business Journal recently hosted a roundtable discussion to tackle all things small business financing. The discussion, moderated by Mike Kinderman, loan officer with Twin Cities-Metro Certified Development Company, featured panelists Kim Storey, director of SBA lending at Highland Bank, Adam Rao, owner of Triple20, Angie Trocke, commercial lender at Highland Bank, Dan Kolar, owner of CRDN of Minnesota, and Ben Hangge, senior vice president of commercial banking at Highland Bank.

The basics of SBA loans

Mike Kinderman, loan officer with Twin Cities-Metro Certified Development Company, kicked off the conversation by asking about key eligibility requirements of United States Small Business Administration (SBA) loans, which are loans that are backed by the SBA that help small businesses get access to funding through partnerships with lenders.

Kim Storey, director of SBA lending at Highland Bank, said two of the top eligibility requirements for qualifying for an SBA loan are the business must be a for-profit entity operating in the U.S., and 100% of the business’ ownership must be U.S. citizens or U.S. nationals residing in the country.

“The business also must meet specific small business size standards, demonstrate credit worthiness and show a need for financing,” Storey said. “Also, generally, borrowers must have reasonable owner equity, good character, and have the ability to repay the requested loan.”

Storey added that the actual SBA loan is quite flexible. Most of the financing Highland Bank provides is for working capital, equipment, and business or real estate purchases, although Storey said, in certain circumstances, refinancing existing debt is another eligible use of proceeds.

Angie Trocke, VP and Commercial Banker at Highland Bank, said that the typical SBA financing structure will look different depending on what the money is being used for, whether it is for buying a business, buying real estate, buying equipment, or building out space.

Despite the difference in what an SBA loan can be used for, Trocke added that a minimum of 10% cash equity tends to be the normal amount, regardless of what the financing is for.

Trocke further noted that, when qualifying for SBA loans, one of the most critical financial benchmarks is the borrower’s ability to repay, as reflected in key cash flow metrics, such as the debt service or fixed charge coverage ratios.

When it comes to cash flow, Trocke said it can either be historical or projection-based, and can be a combination of the two, depending on the length of time the business has been in operation. Generally, the SBA will look at a three-year period of cash flow when deciding to grant a loan.

A new development that Storey anticipates becoming a large player in SBA loans are Manufacturer’s Access to Revolving Credit (MARC) Loans, which is a program that launched in late 2025.

Storey said these types of loans provide financing to small, U.S.-based manufacturing businesses, with the program offering flexible, working capital up to $5 million to help manufacturers manage demand. Loans can feature a 10-year revolving line of credit that converts to a term loan.

“I foresee there will be interest in the MARC loan program, as the manufacturing industry struggles with tariffs, supply chain disruptions, and inflationary costs into 2026,” Storey said.

What makes a bank want to finance a business?

Ben Hangge, Senior Vice President and Commercial Banking Manager at Highland Bank, offered up “4 C’s of Credit” as to what makes a business attractive to banks for financing.

The 4 C’s are:

Cash Flow: Banks look for businesses with robust cash flow, ensuring it is sufficient to cover debt obligations, fund growth initiatives, and support capital expenditures. The ability to generate consistent, predictable cash flow is a primary indicator of financial health and repayment capability.

Collateral: Adequate collateral is another key factor. Banks seek assets that can secure the loan, reducing their risk exposure. However, in cases where collateral is limited, other positive attributes may help mitigate this requirement.

Capital: Capital represents the equity reflected on the business’s balance sheet, the net worth of owners or guarantors, or cash investment in new ventures such as acquisitions. Sufficient capital demonstrates a commitment to the enterprise and provides a financial cushion for unforeseen circumstances.

Character: Beyond financial metrics, banks also evaluate the trustworthiness, reliability, and credit history of business owners. A strong track record of responsible financial management and repayment is essential for establishing credibility.

Hangge added that industry specific and broader macroeconomic factors also contribute to what makes a business attractive to banks. When assessing an opportunity, he considers a range of questions tailored to these perspectives to ensure a thorough evaluation of the business.

From an industry perspective, Hangge tends to ask questions such as:

Is the industry experiencing growth?

Are there supplier dependency or customer concentration risks?

Is there artificial intelligence or obsolescence risk?

Is the industry fragmented or are there barriers to entry?

Are there opportunities for economies of scale?

Any regulatory or compliance risks?

Are the end customers healthy and is there potential to diversify revenue streams within this space?

From a macroeconomic perspective, Hangge evaluates broader questions, such as:

How sensitive is the business to different economic cycles?

Could geopolitical tensions impact business operations?

Are there supply chain or trade disruptions that may affect the company or its industry?

Could tariffs, inflation, or interest rates affect the industry or business?

Are there labor market or demographic trend concerns?

If a business has shortcomings that may impact their ability to obtain a loan, Hangge said the SBA program is a great way to help “both businesses and banks find ways to get things done that might not otherwise get done.”

“The SBA program is an excellent way to mitigate many of those shortcomings,” Hangge said. “It can help extend amortization schedules to create more cash flow flexibility if that’s a need. It can mitigate collateral shortfalls, it can help bridge capital or down payment gaps, and it can help mitigate some industry or economic concerns that a bank might have about a business.”

What business owners can provide

Kinderman continued the conversation along the same vein by asking what business owners can give to banks to make the entire process of obtaining financing easier.

Adam Rao, owner of Triple20, said business owners tend to focus mostly on growth and the top line when, in reality, cash flow is “everything.”

“Cash is king when it comes to how banks operate, how banks think, how debt actually functions and works,” Rao said.

Due to this, Rao said the number one thing business owners can provide to banks in order to improve the likelihood of securing funding is being able to show how cash flows in and out of the business and how an owner will be able to make payments.

“Instead of focusing on revenue or anything that’s non-cash, like net income even on your typical income statement, EBITDA is really the key metric,” Rao said.

Dan Kolar, owner of CRDN of Minnesota, said when he has sought financing, it was crucial for him to have basic financial statements prepared, which all comes back to maintaining a good relationship with the accountant one’s organization works with.

Kolar added that when small business owners do not have a strong relationship with their accountant, especially if they are third-party, things take longer and are not as clear, which can impact how a business looks to a bank.

“I think just having a good relationship with the accountant and making sure your financial statements can be very clear and concise is one of the most important things,” Kolar said.

Kinderman, as a lender himself, echoed this sentiment, saying it is impossible for someone to be an expert in everything.

“I appreciate when business owners we work with recognize they might have an area of weakness and then they lean on their partners,” Kinderman said. “They lean on those trusted partners like a CPA or accountant to make sure that they are still getting the information needed to be able to have a positive impact on the operations of their company.”

Recent changes in SBA lending

Kinderman shifted the conversation over to the kinds of changes that exist within SBA lending and how they are affecting small businesses.

Storey said one of the biggest changes in SBA lending has been the underwriting criteria becoming more standardized and consistent across the program. She added that the Standard Operating Procedures (SOP) was released in 2025 restored several policies that had been in place in previous years.

“As a result of that, lenders are analyzing addbacks, reviewing broker adjustments a little more closely, focusing on global debt service coverage ratios, particularly when you’re looking at acquisitions and real estate financing,” Storey said.

She continued by adding that there has been a re-emphasis on 10% being the minimum equity injection, which is “absolutely shaping deal structure today, particularly for new businesses.”

Ownership structure is also something that has recently changed, since SBA loans now have a citizenship requirement in order to be eligible, according to Storey.

“That has become more front-of-the-line due diligence for bankers and could affect deal structure,” Storey said. “There could potentially be changes in ownership if there isn’t a party that might qualify now that did maybe even a month ago.”

As the SBA landscape continually shifts, Storey said it is crucial for banks to support their clients through these changes.

Highland Bank has invested in having a dedicated team that is in charge of managing the regulatory compliance and risk management that goes along with SBA lending, according to Storey.

She continued that Highland Bank tries to leverage technology to support a more streamlined SBA workflow and consistently pre-screens clients to identify potential issues upfront.

Challenges during the SBA process and the benefits of a Preferred Lender

Trocke said a common misconception that she runs into with clients when starting the SBA process is that it takes too long and is too difficult. She said this misunderstanding is one of the biggest challenges borrowers face when looking to obtain an SBA loan.

While it is a large obstacle, Trocke said the best way to overcome it is by making sure individuals choose an “SBA Preferred Lender,” which is an SBA-authorized bank that can approve loans in-house.

“A Preferred Lender is going to make the process quicker, smoother, easier and is really not a whole lot different than any sort of conventional financing,” Trocke said.

Storey added that Preferred Lenders have the authority to make credit decisions on behalf of the SBA, which streamlines the entire process.

“That’s really, really important for a company to understand because all of the information that we are requesting is getting us to the point of being able to make a credit decision,” Storey said. “The end result is higher approval rates for borrowers, and a quicker more streamlined process from beginning to end.”

Kolar and Rao, who both work with Highland Bank for their businesses’ loans, said a highlight of working with a Preferred Lender was the streamlined process, which made everything easier in the long run.

“Banks and business owners have to treat each other as partners,” Rao said. “A bank can’t do what the bank does without us and we can’t do what we do without banks. So finding the best bank partner that you can absolutely should be the top priority of every business owner. Then once you have one, never let them go.”

Another misconception Trocke has seen with clients is that pledging personal assets is an SBA loan-specific requirement, when, in actuality, that is not much different from conventional financing. Also, while pledging personal assets is a possibility for SBA loans, it is not always a requirement.

“That’s one of the challenges for a lot of small business owners when they seek financing is the thought that they may have to pledge their home as collateral sometimes or their personal assets,” Kinderman said. “But that’s what a lot of small business owners do when they get started. It’s part of taking that risk, that leap, and making an investment in themselves and in their company.”

Are you prepared to buy a business?

Kinderman then zoomed out the conversation by asking what are signs that an individual is ready to buy a business and potentially start looking at loans.

Rao said it all comes down to the mindset.

While some people think of business ownership as purchasing an asset, Rao said there is a difference in mentality of an entrepreneur, which is that “buying a business can be just as entrepreneurial as starting one from scratch.”

Rao continued that while it can still work for someone to buy a business, keep it the same, and “tweak around the edges,” people that bring an entrepreneurial mindset to the table and are able to see growth potential and take on risk to make that happen often get more interesting opportunities.

“That’s where I think SBA is really great,” Rao said. “You do have this ability to have a longer time frame, less equity in, both the bank and you as the purchaser are pushing some of the risk onto the government. So you have this opportunity to kind of create partnership with your bank and actually get deals done and see the future of something in a different way than when we’re really trying to make sure all the cash flow statements look exactly the way that they need to or whatever the case is.”

Understanding risk in the SBA landscape is also crucial, according to Rao. It’s important for business owners to know the difference between fear and risk in the industry and how one can be afraid of a business outcome but that does not mean there is risk involved.

“Good entrepreneurs are the ones who understand what the real risks are, and then you do everything you can to mitigate them,” Rao said. “That’s exactly how banks are trying to think as well. Good banks are trying to make opportunities happen.”

Kolar added onto this topic, saying that before he considered buying CRDN, he immersed himself in the actual work to see if it was something he wanted to do every single day.

“One of the most important things and one of the first things is to just dive into the business,” Kolar said. “Shadow somebody. If you can, just get into the business, into the nitty gritty, deliver the clothes, work the machines, see if you could do it for a long time. That was one of the first things I did and it was for sure the best thing that I did.”

Kolar added that once an individual realizes they can do the job, they should start looking at the barriers to entry in that specific industry. He said one of the first things he looked at was industries that had slightly higher barriers to entry that required some expertise, since that improved the likelihood of the business being more secure.

“It makes the business a little bit more attractive and a little bit more secure if there are some barriers to entry,” Kolar said.

What sets Highland Bank apart

In addition to its status as an SBA Preferred Lender, Highland Bank stands out for two primary reasons, according to Hangge.

First, Highland Bank is known for its collaborative approach. Unlike institutions that operate within rigid credit parameters, the bank adopts a flexible process, actively seeking and incorporating customer feedback to structure the best deal for all parties involved.

This emphasis on collaboration also provides valuable learning opportunities for customers, especially those new to the financing process.

“Sometimes, customers request certain terms or structures that may not serve their business well in the long run. Our process involves understanding their reasoning, discussing the potential implications, and educating them on alternative approaches that may better support their future success,” Hangge explained. This advisory role is considered a crucial component of the bank’s service philosophy.

The second distinguishing factor is Highland Bank’s expedited decision-making process, high level of transparency, and the direct access clients have to senior leadership within the organization.

“Our clients have direct lines of communication to everyone, from the bank’s owner and CEO to the chief credit officer, ensuring clear and collaborative discussions whenever necessary,” Hangge noted.

This level of accessibility accelerates the lending process and enhances client confidence throughout the relationship.

Above all, Hangge emphasized the rewarding nature of working closely with a diverse group of business owners and entrepreneurs and supporting them as they pursue and achieve their business objectives.

“SBA lending is about people, the relationships that we have, and just helping dreams move forward,” Storey said. “So any way that we can do that efficiently, effectively is kind of the end goal.”

Spring is a season of renewal—longer days, fresh starts, and the perfect time to take a closer look at your finances. That’s why April, recognized as Financial Literacy Month, is an ideal time to brush up on smart money habits and plant the seeds for long-term financial confidence.

Whether you’re planning home projects, reorganizing your budget, or looking for ways to make your money work harder, a few thoughtful financial decisions now can help you grow stability all year long.

Start with the Basics: Financial Literacy That Grows With You

Financial literacy is about understanding how everyday financial choices—saving, borrowing, spending, and planning—work together. When you have the right tools and knowledge, you can make informed decisions that support both short-term needs and long-term goals.

This spring, consider:

Reviewing your monthly budget and cash flow

Exploring smarter ways to pay for large or unexpected expenses

Choosing accounts that reward responsible financial habits

Small changes today can lead to meaningful growth tomorrow.

Using Your Home’s Equity Wisely This Spring

Spring often brings a list of projects and priorities—home improvements, consolidating higher-interest debt, or simply creating flexibility for future needs. One option many homeowners consider is tapping into their home’s equity.

A Home Equity Line of Credit (HELOC) allows you to borrow against the equity you’ve built in your home, giving you access to funds as you need them rather than all at once. This flexibility can make a HELOC a helpful tool for managing planned or ongoing expenses—especially when used thoughtfully and responsibly.

Make Everyday Banking Work Harder with Kasasa Cash

Financial literacy isn’t just about borrowing wisely—it’s also about choosing accounts that reward smart, everyday behavior.

A Kasasa Cash® checking account is designed to do just that. By completing simple monthly activities you’re likely already doing—like using your debit card or receiving electronic statements—you can earn competitive rewards and nationwide ATM fee refunds.

One unique way to qualify for rewards is through the loan bundle option, which includes having an active home equity loan or line of credit with Highland Bank. That means pairing the right loan with the right checking account could help you maximize benefits while keeping your finances streamlined.

A Smarter Pairing for Spring Financial Growth

When used together, tools like a HELOC and a Kasasa Cash account can support a more intentional approach to money:

Flexibility to fund projects or manage expenses as they arise

Rewards for maintaining healthy financial habits

Simplicity by keeping your banking and borrowing connected

It’s not about doing more—it’s about making smarter choices with what you already have.

Plant the Seeds for a Stronger Financial Future

Financial Literacy Month is a reminder that knowledge is one of your most powerful financial tools. This spring, take time to ask questions, explore your options, and choose solutions that align with your goals.

Whether you’re refreshing your budget, planning for home projects, or looking to earn more from your everyday banking, our team is here to help you grow with confidence—this season and beyond.

Your home is more than just where life happens—it’s also one of your most valuable financial tools. As you build equity over time, that value can open the door to new possibilities. A Home Equity Line of Credit (HELOC) lets you turn your equity into opportunity, giving you flexible access to funds when you need them most.

As spring rolls into summer, many homeowners start thinking about what’s next—home improvement projects, outdoor upgrades, or simply getting ahead financially. A HELOC can help you take action now, without putting your plans on hold.

What Is Home Equity?

Home equity is the difference between your home’s current market value and what you still owe on your mortgage. With every mortgage payment you make—and as your home’s value grows—your equity increases. Over time, that equity becomes a powerful resource you can use to support your goals.

What Is a HELOC—and How Is It Different from a HEIL?

Both a Home Equity Line of Credit (HELOC) and a Home Equity Installment Loan (HEIL) allow you to borrow against the equity you’ve built in your home—but they work in very different ways.

A HELOC gives you access to a line of credit based on your home’s equity. You’re approved for a maximum amount, but you don’t have to use it all at once. Instead, you can borrow what you need, when you need it, and only pay interest on the amount you actually use. This flexibility makes a HELOC a great option for ongoing or unpredictable expenses—like tackling spring and summer home projects in stages, covering costs as they come up, or keeping funds available “just in case.”

A HEIL, on the other hand, provides a one-time lump sum of money with a fixed interest rate and set monthly payments. It’s often a good fit for a single, large expense with a clear price tag—such as a major renovation or a specific financial goal where you know exactly how much you need upfront.

In short:

A HELOC offers flexibility and access over time.

A HEIL offers predictability with a fixed payment schedule.

If you like the idea of turning your equity into opportunity—and want the freedom to fund projects, plans, or unexpected expenses as life happens—a HELOC can be a smart, adaptable solution.

How Can You Use a HELOC?

One of the biggest advantages of a HELOC is how versatile it is. Many homeowners use a HELOC to get ahead of spring and summer projects—like updating a kitchen, replacing windows, finishing a basement, or tackling outdoor improvements before the busy season begins.

Others use it to cover larger life expenses, such as college tuition, medical bills, or consolidating higher-interest debt. And for some, a HELOC simply offers peace of mind—a financial safety net that’s there when the unexpected happens.

Whatever your goal, a HELOC gives you the freedom to decide how and when your funds are used.

Make the Most of What You’ve Built

You’ve worked hard to build equity in your home—now it’s time to put it to work for you. Whether you’re planning seasonal upgrades, managing major expenses, or simply want more financial flexibility, a HELOC can help you move forward with confidence.

Connect with our HELOC experts today or learn more about our limited-time HELOC special.

Highland Bank’s VP, Commercial Banker, Joe Veliz, joins panel discussion hosted by VR Mergers & Acquisitions, Business Appraisal, MN. This session is designed for business leaders seeking clear insight on how to make key banking and lending decision in what is panning out to be a volatile year.

Simple Ways to Save, Protect, and Feel More Confident

If improving your finances is one of your goals for 2026, you’re not alone. For many people, money isn’t about having all the answers—it’s about feeling a little more prepared, a little less stressed, and more confident about the future.

The good news? You don’t need a complete financial overhaul to make progress this year. A few smart habits, paired with today’s financial trends, can make a meaningful difference over time.

Saving Feels Easier When Your Money Works in the Background

After years of low interest rates, everyday banking accounts are doing more than just holding your money. Many checking and savings options now offer ways to earn higher interest, cash back, or rewards simply by using your account the way you already do.

That’s where Highland Bank’s Kasasa® Checking accounts can support your goals—earning rewards while you handle everyday spending like debit card purchases and online banking.

Try this:

Keep the money you use regularly in an account that rewards everyday activity.

Pair your checking account with a high-yield savings account for longer-term goals.

Let your money earn something—even while you’re just living life.

Sometimes the best progress comes from making small improvements to what you already are doing.

Let Automation Keep You Consistent

Life is busy, and remembering to move money around every month isn’t always realistic. Automation continues to be one of the easiest ways to stay consistent with saving and spending goals in 2026.

Easy wins:

Set up automatic transfers from checking to savings after payday.

Schedule bill payments to avoid late fees and stress.

Use account alerts to stay informed without having to constantly check balances.

With the right tools in place, your finances can feel more organized—without taking more of your time.

Protecting Your Money Starts with Everyday Habits

As more banking happens digitally, protecting your money has become part of everyday financial wellness.

Simple steps—like account alerts, secure logins, and monitoring transactions—can go a long way. Many modern checking accounts offer built-in features that help you stay aware and in control.

Good habits to build this year:

Review your accounts regularly, even if it’s just a quick check.

Enable multi-factor authentication (MFA) where available. MFA adds an extra layer of security by requiring more than just a password—like a code sent to your phone—to verify it’s really you.

Be cautious with unexpected messages asking for personal information.

A little prevention now can save a lot of worry later.

Budgeting Without the Guilt

Budgeting doesn’t have to mean cutting out everything you enjoy. In reality, it’s about understanding where your money goes so you can make choices that align with your priorities.

A checking account that’s easy to manage—especially one with online and mobile tools—can help you track spending patterns and adjust as needed.

A realistic approach:

Start by tracking spending for one month—no judgment.

Group expenses into simple categories: needs, savings, and fun.

Make small adjustments that feel sustainable.

Progress sticks when it feels doable.

Small Changes, Real Confidence

Being “better with money” in 2026 isn’t about big sacrifices or complicated strategies. It’s about creating systems that work for your real life— choosing accounts that support your goals , saving a little, and protecting what you earn.

Whether it’s automating savings, using a checking account that rewards everyday activity like Kasasa® Checking, or simply paying closer attention to your spending, every small step adds up.

Confidence grows when your money starts working with you, not against you. Wherever you’re starting from, 2026 is a great year to build habits that support both today’s needs and tomorrow’s goals.

Every day, thousands of people fall victim to fraudulent emails, texts and calls from scammers pretending to be their bank, a loved one, the government or law enforcement. And in this time of expanded use of online and mobile banking, the problem is only growing. In fact, the Federal Trade Commission’s report on fraud estimates that American consumers lost a staggering $12.5 billion to phishing scams and other fraud in 2024 — an increase of 25% over 2023.

These criminals are skilled at tricking you— convincing you to trust them, pay them and act fast. It’s time to snap out of it.

At Highland Bank, we’re committed to helping you spot scams. We’ve joined the American Bankers Association and banks across the country in a nationwide effort to help you realize when you’re under a scammer’s trance and snap out of it so you avoid losing your money.

We want every bank customer to become a scam-spotting pro — and stop these criminals in their tracks. If something feels off, stop, take a breath and trust yourself.

Five red flags to look out for:

You’re pressured to log into or send money with payment apps — Snap out of it.

You’re contacted out of the blue, asked to act immediately and keep it a secret — Snap out of it.

You get a text that includes a suspicious link — Snap out of it.

You’re emailed an attachment that you weren’t expecting — Snap out of it.

You’re asked for personal information like your PIN number, passwords or Social Security number — Snap out of it.

You’ve probably seen some of these scams before. But that doesn’t stop a scammer from trying. For tips, videos and an interactive quiz to help you keep criminals at bay, visit BanksNeverAskThat.com. And be sure to share the webpage with your friends and family.

Information provided by the American Banker’s Association

SBA’s online learning programs are designed to empower and educate small business owners every step of the way!

Did you know that the Small Business Administration (SBA) offers FREE online courses to help you plan, launch, manage, market, and grow your business?

Whether you’re looking to start a small business or expand your current one, SBA’s digital learning platform has everything you need to educate yourself on entrepreneurial best practices and available financing options.